(Picture credit: "Home Alone" movie)

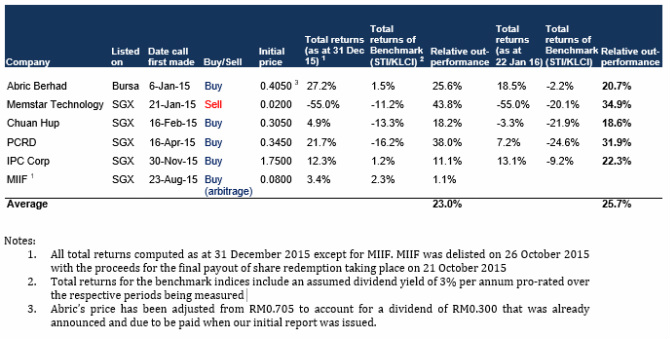

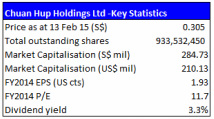

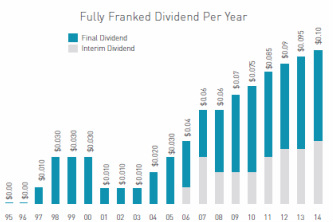

Following PCRD’s special dividend announced beginning this month, another one of our earlier deep value picks, Chuan Hup Holdings (“CHH”), has also followed suit by proposing an impressive payout of its own. CHH is aiming to distribute a massive S$0.09 per share to its shareholders, equivalent to a 26.5% yield based on its last closing price of S$0.34.

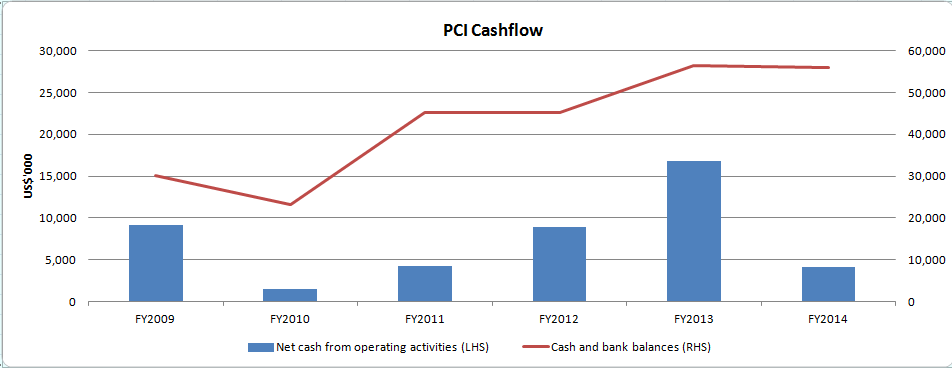

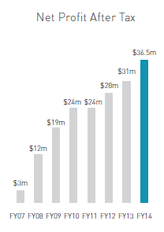

This follows the Company's decision in January to divest its entire 76.7% stake in cash-rich subsidiary PCI Ltd for S$203 million to private equity outfit, Platinum Equity Advisors. The deal is subject to the approvals of:

However, with the undertaking from CHH to vote in favour of the scheme, the Peh family controlling more than 50% of CHH shares, as well as the sweetener of the dividend payout for CHH shareholders, we expect both sets of shareholders to vote overwhelmingly in favour of the deal.

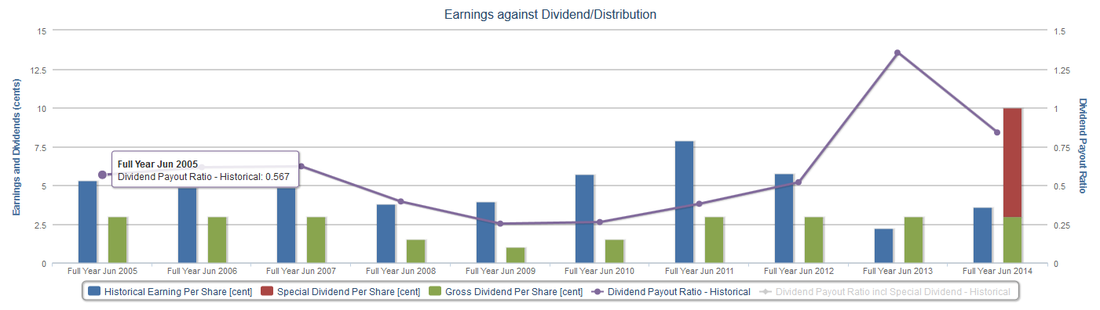

Tracing back to the time we issued our initial report in early 2015 when CHH’s share price was trading at S$0.305, the minority-friendly Company has either proposed or distributed a total of S$0.17 in dividends to date.

In this regard, we commend the Company’s efforts to consistently reward its shareholders and urge more cash-rich companies to follow suit.

Related: http://stockresearchasia.com/latest-recommendations/chuan-hup-holdings-ltd-deep-value-emerging

Following PCRD’s special dividend announced beginning this month, another one of our earlier deep value picks, Chuan Hup Holdings (“CHH”), has also followed suit by proposing an impressive payout of its own. CHH is aiming to distribute a massive S$0.09 per share to its shareholders, equivalent to a 26.5% yield based on its last closing price of S$0.34.

This follows the Company's decision in January to divest its entire 76.7% stake in cash-rich subsidiary PCI Ltd for S$203 million to private equity outfit, Platinum Equity Advisors. The deal is subject to the approvals of:

- PCI shareholders under a court-sanctioned Scheme of Arrangement pursuant to the Companies Act of Singapore; as well as

- CHH shareholders in an EGM to be held in the coming weeks.

However, with the undertaking from CHH to vote in favour of the scheme, the Peh family controlling more than 50% of CHH shares, as well as the sweetener of the dividend payout for CHH shareholders, we expect both sets of shareholders to vote overwhelmingly in favour of the deal.

Tracing back to the time we issued our initial report in early 2015 when CHH’s share price was trading at S$0.305, the minority-friendly Company has either proposed or distributed a total of S$0.17 in dividends to date.

In this regard, we commend the Company’s efforts to consistently reward its shareholders and urge more cash-rich companies to follow suit.

Related: http://stockresearchasia.com/latest-recommendations/chuan-hup-holdings-ltd-deep-value-emerging

RSS Feed

RSS Feed